Georgia’s B2B Revenue Guard: Elite Account Reconciliation for the Empire State

In Georgia’s high-stakes commercial landscape, cash flow is the difference between scaling a Midtown fintech firm and stalling out on the I-75 industrial corridor. From the heavy-lift logistics surrounding the Port of Savannah to the precision manufacturing hubs of Dalton, an unpaid invoice isn’t just a number—it’s a disruption to your supply chain. At CA-USA, we don’t “collect debt.” We deploy an elite Account Reconciliation Team to protect your professional reputation while securing the capital you’ve already earned.

CA-USA provides a low cost, compliant, reputation-safe approach, equipped with all 50-state collections license, offering free credit reporting, free litigation, free bankruptcy scrubs, and zero onboarding fees. Secure – SOC 2 Type II compliant. Over 2,000 online reviews rate us 4.85 out of 5. Over 20 years experience, delivering excellent B2B collection results.

Need a Commercial Collection Agency? Contact us

Performance-Based Precision

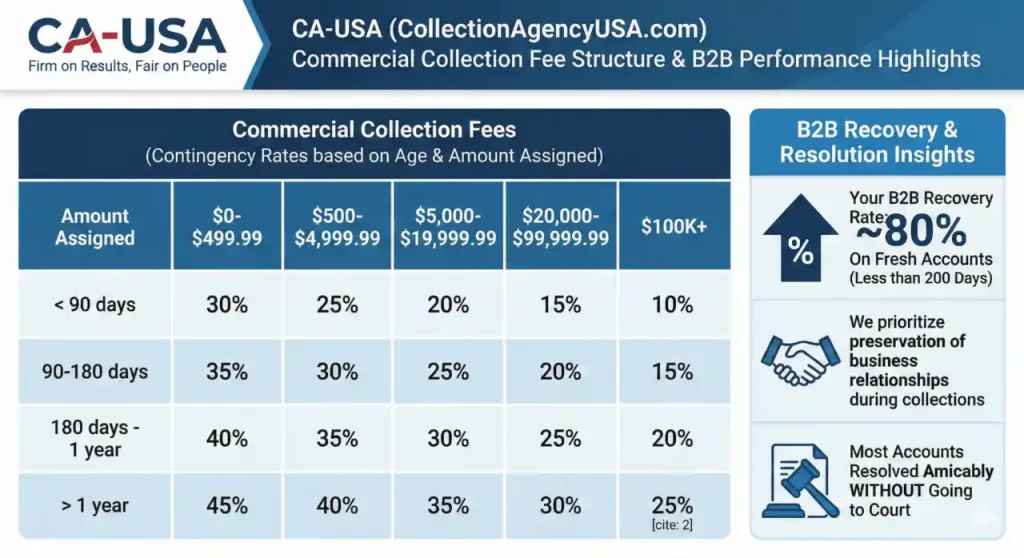

We operate on a strictly Contingency-Only Model. Our interests are locked to yours: if we don’t recover your funds, you don’t pay a dime. Fees range from 10% to 45%, meticulously calculated based on the balance age, volume, and case complexity. We provide this transparent pricing in advance, ensuring that younger, high-value accounts receive our most aggressive, low-friction rates.

The “Firm on Results, Fair on People” Edge

Hard-line tactics often trigger defensive litigation or “review-bombing” that stains your brand. We prioritize Amicable Mediation. By engaging debtors as human beings rather than file numbers, we resolve most accounts without the expense of a courtroom. However, we back our empathy with an 80% recovery rate on fresh commercial accounts (under 200 days). We don’t just ask for payment; we negotiate a resolution that often keeps the vendor relationship intact for future Georgia business.

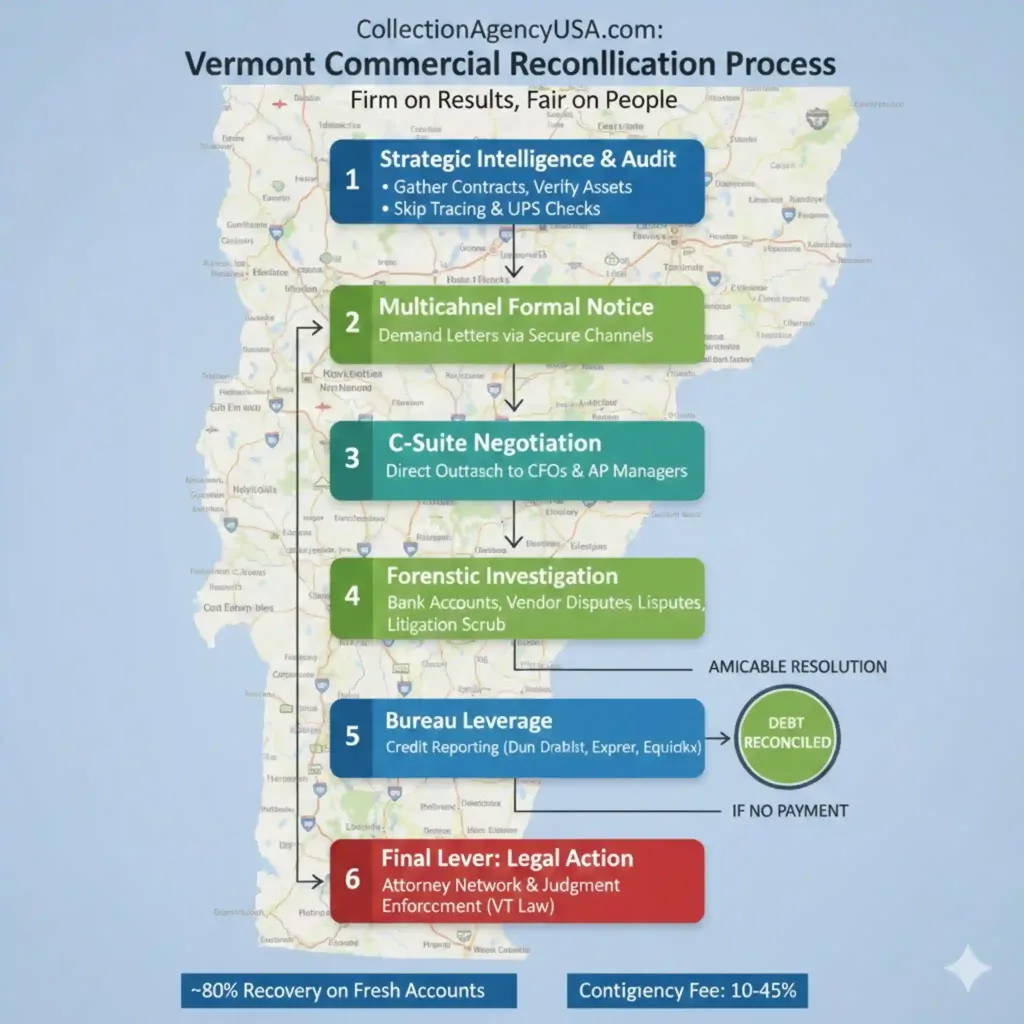

Commercial Reconciliation Workflow

-

Contractual Audit & Asset Intel: We verify corporate assets and audit UCC filings to ensure the debtor has the liquidity to pay before we even make the first call.

-

Executive-Level Outreach: We bypass the “check is in the mail” gatekeepers. Our team negotiates directly with CFOs and Controllers who have the authority to release funds.

-

Digital Multi-Channel Demands: We utilize high-velocity email and text strategies to establish an immediate, undeniable paper trail.

-

Forensic Investigation: Our Litigation Scrub filters out high-risk accounts, while our deep-dive skip tracing locates hidden corporate assets across the state.

-

The Credit Reporting Lever: As a powerful non-legal motivator, we report delinquencies to Dun & Bradstreet, Experian Business, and Equifax Commercial, effectively freezing the debtor’s ability to secure new credit or favorable vendor terms.

-

Judgment Enforcement: When mediation hits a wall, we activate our nationwide network of attorneys to pursue legal action and asset seizure.

Georgia Legal & Compliance Guardrails

Georgia’s B2B landscape is governed by specific statutes—from the six-year statute of limitations on written contracts (O.C.G.A. § 9-3-24) to the nuances of the Georgia Fair Business Practices Act. We handle the complexity for you. Every call is recorded and reviewed to ensure 100% compliance, insulating your company from the liability of “rogue” collection tactics. We provide USPS address verification, Bankruptcy checks, and Spanish-speaking bilingual support to ensure no account slips through the cracks of the Peach State’s diverse economy.

The Strategic B2B “Red Flags” in Georgia

-

The Seasonal Stalling: In Georgia’s agricultural and tourism sectors, debtors often try to “float” their debt until the next peak season. We intervene early to ensure your invoice is top-of-pile.

-

The Logistics Loophole: Near the Savannah or Brunswick ports, firms often blame “customs delays” for non-payment. Our forensic team verifies these claims in real-time.

-

The Ghosting Startup: Atlanta’s tech scene moves fast. If a firm stops communicating, we deploy immediate skip tracing to protect your interest before they dissolve or rebrand.

Commercial Strategy FAQ

Can we collect from a business owner personally?

In Georgia, if an owner signed a Personal Guarantee, they are personally on the hook. Furthermore, in Sole Proprietorships or Partnerships, there is no legal “shield” between business debt and personal assets. We also look for Fraudulent Transfers—where owners move money to avoid creditors—which can be challenged in court.

Why shouldn’t my internal team handle this?

Every hour your team spends playing “debt detective” is an hour they aren’t closing new Georgia business. Our reconciliation team acts as a professional buffer, allowing your employees to maintain a positive, sales-focused relationship while we handle the “tough talk” of reconciliation.

Recover your Business Debts? Contact us