You restored the property. You documented everything, managed the crew, coordinated with the adjuster, and delivered the work. The invoice went out. And now — silence.

Restoration companies are built to respond fast and work clean. Chasing payments is neither. What a professional collection agency brings to the table isn’t just persistence — it’s a set of capabilities your internal team structurally cannot replicate.

| CA-USA provides a low cost, compliant, reputation-safe approach, equipped with all 50-state collections license, offering free credit reporting, free litigation, free bankruptcy scrubs, and zero onboarding fees. Secure – SOC 2 Type II compliant. Over 2,000 online reviews rate us 4.85 out of 5. Over 20 years experience , delivering excellent collection results. Need a Collection Agency? Contact us |

Omnichannel Outreach at the Right Cadence

Phone calls alone don’t move accounts anymore. Agencies run a legally compliant mix of mail, phone, email, and text — timed to maximize response without crossing into harassment under the CFPB’s seven-call rule. Every contact is logged. Your receptionist making follow-up calls between scheduling jobs isn’t a system. It’s improvisation — and the recovery rates reflect the difference.

Credit Reporting as a Recovery Lever

When permitted by law and account type, reporting a delinquent account to Experian, Equifax, or TransUnion changes debtor behavior faster than repeated calls. For homeowners and property managers who care about their credit standing, a collection entry creates real urgency. Restoration companies cannot report to credit bureaus directly. Only licensed agencies with established reporting agreements can.

Neutral Third-Party Distance

There’s something no software solves: the discomfort of a restoration owner calling a longtime customer to collect a disputed invoice. The conversation is loaded — it risks the relationship, the referral, the online review. A collection agency removes that friction entirely. The debtor is no longer saying no to you personally. They’re navigating a professional process with a neutral party who has no emotional stake — and debtors who stalled for months with internal follow-up often resolve within weeks once that dynamic shifts.

Documentation That Holds Up

Every contact attempt, payment promise, and dispute is logged and timestamped by a collection agency. That paper trail matters if an account escalates to litigation. A call log in a spreadsheet — or in someone’s memory — doesn’t hold up the same way.

The Point Most Companies Miss: Time Is the Enemy

Recovery rates drop significantly after 90 days. Most restoration companies wait far longer than that before referring accounts, often because internal staff is already stretched. Every week an account sits unworked is a week the debtor grows more comfortable not paying. Earlier assignment isn’t just better strategy — it’s what the data consistently shows.

Your People Were Hired to Restore Properties

Every hour your project coordinator spends chasing an invoice is an hour not spent estimating new work or retaining the customers who do pay. Collections is a specialized function — treating it as something existing staff can absorb quietly is how restoration companies end up with six figures in aging receivables and no clear path to recovery.

Skip Tracing: Finding People Who Don’t Want to Be Found

Property owners move. Contact information goes stale. A homeowner who signed a work authorization after a flood may have a disconnected number and a new address by the time the dispute drags on. Your staff can Google someone — that’s not skip tracing. Licensed agencies access credit header data, utility records, and proprietary address history databases unavailable to the general public. When a debtor goes quiet, professionals find them. Your team cannot.

Bankruptcy and Litigation Screening

Before investing resources in an account, you need to know if it’s worth pursuing. A debtor who has filed Chapter 7 is legally shielded by an automatic stay — contacting them anyway, even unknowingly, exposes your business to liability. Agencies run bankruptcy checks and litigation screening as standard before any outreach begins, separating productive collection from accounts that carry more legal risk than dollar value.

One More Thing: FDCPA and State Law Compliance Across All 50 States

Federal FDCPA rules govern third-party collectors nationwide — but layered on top are state-specific statutes, contact restrictions, and licensing requirements that shift market to market. A restoration company working across multiple states faces a compliance patchwork that most office administrators simply aren’t equipped to navigate. Agencies handle this daily. Missteps don’t just mean failed collections — they can mean regulatory complaints, consumer protection lawsuits, and review-bomb damage from debtors who know how to weaponize the process.

Involving a collection agency significantly improves recovery rates. The earlier an account is assigned, the more recoverable it becomes.

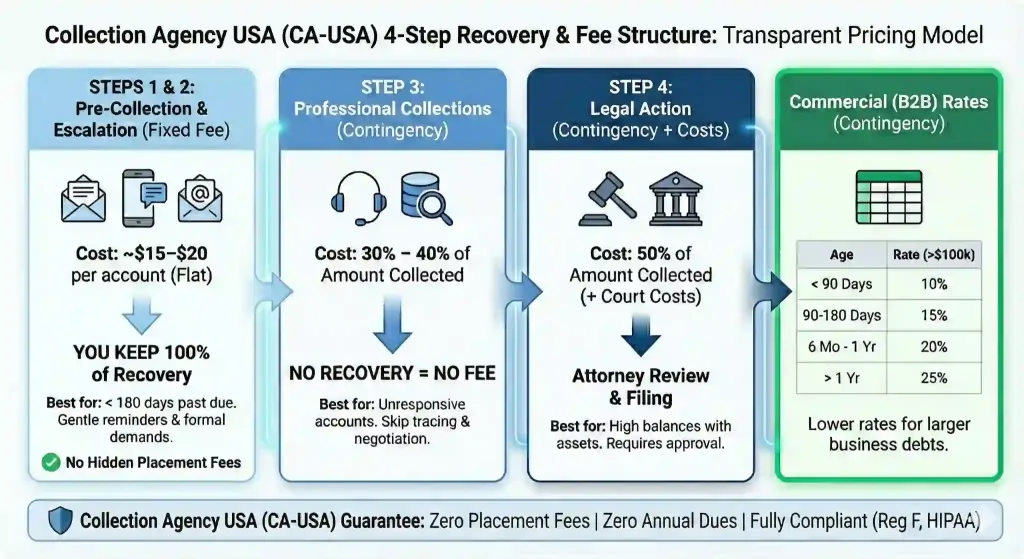

Cost-Effectiveness: The CA-USA Advantage

-

Fixed-Fee Recovery ($15/account): Ideal for early-stage accounts. Debtors pay 100% directly to you.

-

Contingency Service (20%–40%): Performance-based recovery. If we don’t recover your money, you owe us nothing.